1Q25 Optical Component Report

Datacom revenues and shipments slowed, 400ZRx shipments kept Telecom revenue growing for a fourth consecutive quarter.

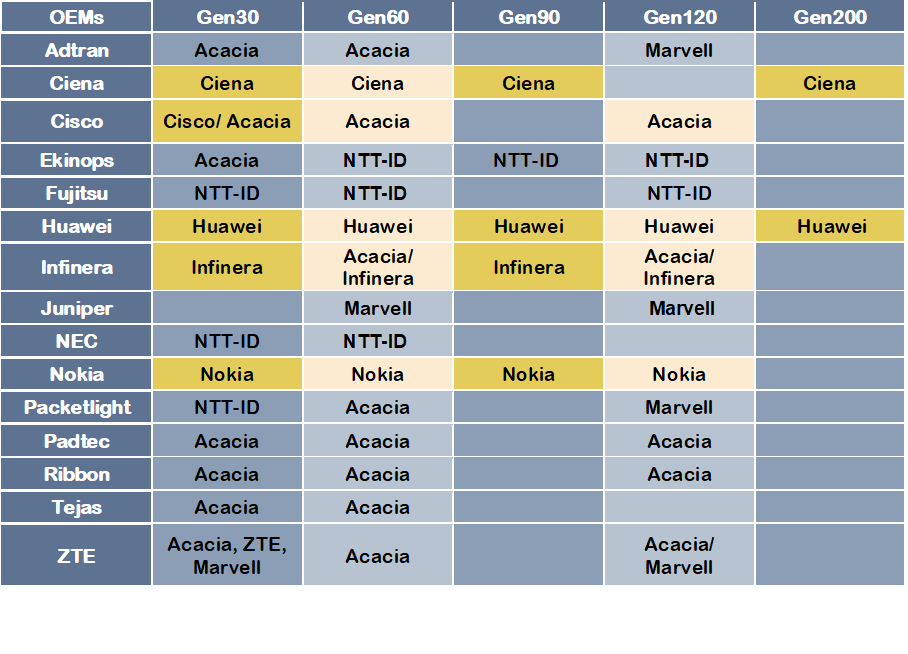

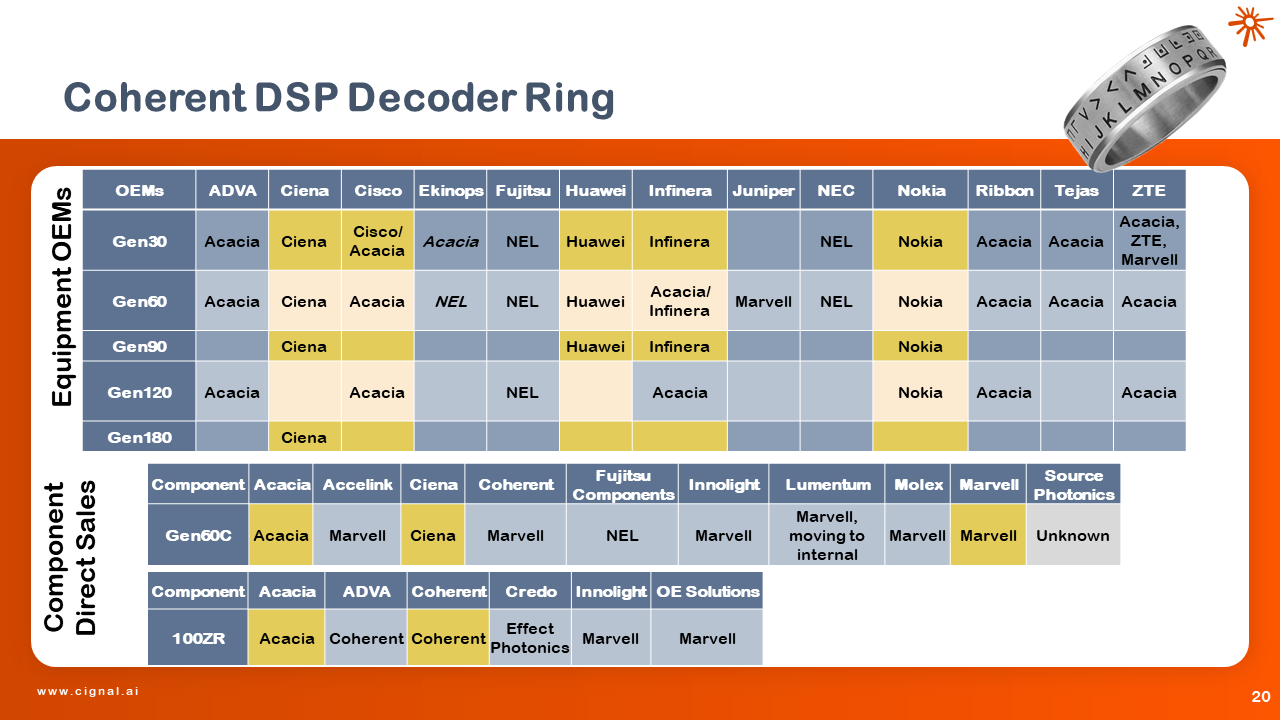

Tracking the Coherent DSP Supply Chain – 2025

Uncovering who uses which DSP, and which DSP vendors ship the most volume.

4Q24 Optical Component Report

Datacom revenue and port shipments stalled this quarter. Telecom revenue recovered from the doldrums based on 400G pluggables.

4Q24 Interim Optical Component Report

Final report will be issued once all Chinese companies complete 4Q24 reporting.

3Q24 Optical Component Report

Datacom revenue more than doubled for the second quarter in a row as AI demand for 400GbE and 800GbE modules continued unabated. Telecom revenue has emerged from the depths of its recent decline.

2Q24 Optical Component Report

Datacom revenue hit new records with a surge in 400GbE shipments and continued growth in 800GbE. Telecom’s only growth area is 400G coherent pluggables.

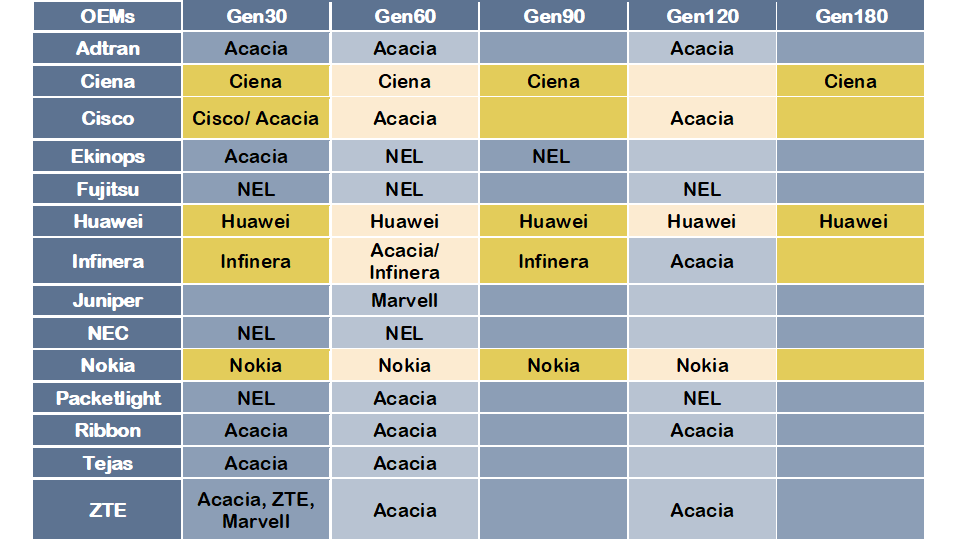

Tracking the Coherent DSP Supply Chain

Uncovering who uses which DSP, and which DSP vendors ship the most volume.

1Q24 Optical Component Report

Datacom revenue and shipments of 400GbE & 800GbE modules hit new records as Telecom struggles to recover.

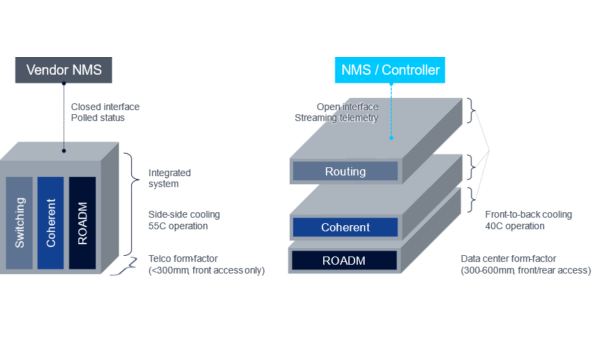

Compact Modular Hardware

This report provides historical information, industry context, and product examples of our classification of Compact Modular systems.

4Q23 Optical Component Report

Telecom revenue has hit the bottom as overwhelming 800GbE demand raises Datacom revenue and shipments.

3Q23 Transport Applications Report

Worldwide DWDM deployed bandwidth declined YoY for the first time.

3Q23 Optical Components Report

Datacom revenues are recovering from the Q1 drop and are poised to explode along with 800GbE shipments in 2024. Telecom revenue continues to lag, as deployed bandwidth declined YoY for the first time this quarter.

2Q23 Optical Components Report

Datacom revenue and module shipments plummeted as inventory adjustment hit hard this quarter.

2Q23 Transport Applications Report

Bandwidth growth and compact modular sales slow as Hyperscalers take their foot off the gas.

1Q23 Transport Applications Report

The Bandwidth Must Flow: Up 39% YoY

1Q23 Optical Components Report

Datacom revenue and module shipments plummeted as inventory adjustment hit hard this quarter.

NGON 2023 Show Report

Observations on IP over DWDM and the Optical Edge

4Q22 Optical Components Report

Datacom and Telecom revenue was up for the year, but headwinds are pushing down forecasts for both revenue and shipments in the first part of 2023.

Tracking the Coherent DSP Supply Chain

Uncovering who uses which DSP, and which DSP vendors ship the most volume.

Optical Components – 4Q22 Preliminary Report

The Optical Components report is expected to release in mid-April. In the meantime, this interim report provides an overview of how quarterly results are trending.