Tracking the Coherent DSP Supply Chain – 2026

Uncovering who uses which DSP, and which DSP vendors ship the most volume. Updated with the latest data from 2025.

4Q25 Optical Component Report

Datacom revenue crossed $6 billion for the quarter and $19 billion for the year as more than 42 million 400G+ datacom modules shipped. Annual Telecom revenue reached new heights as well, up 35% over 2024.

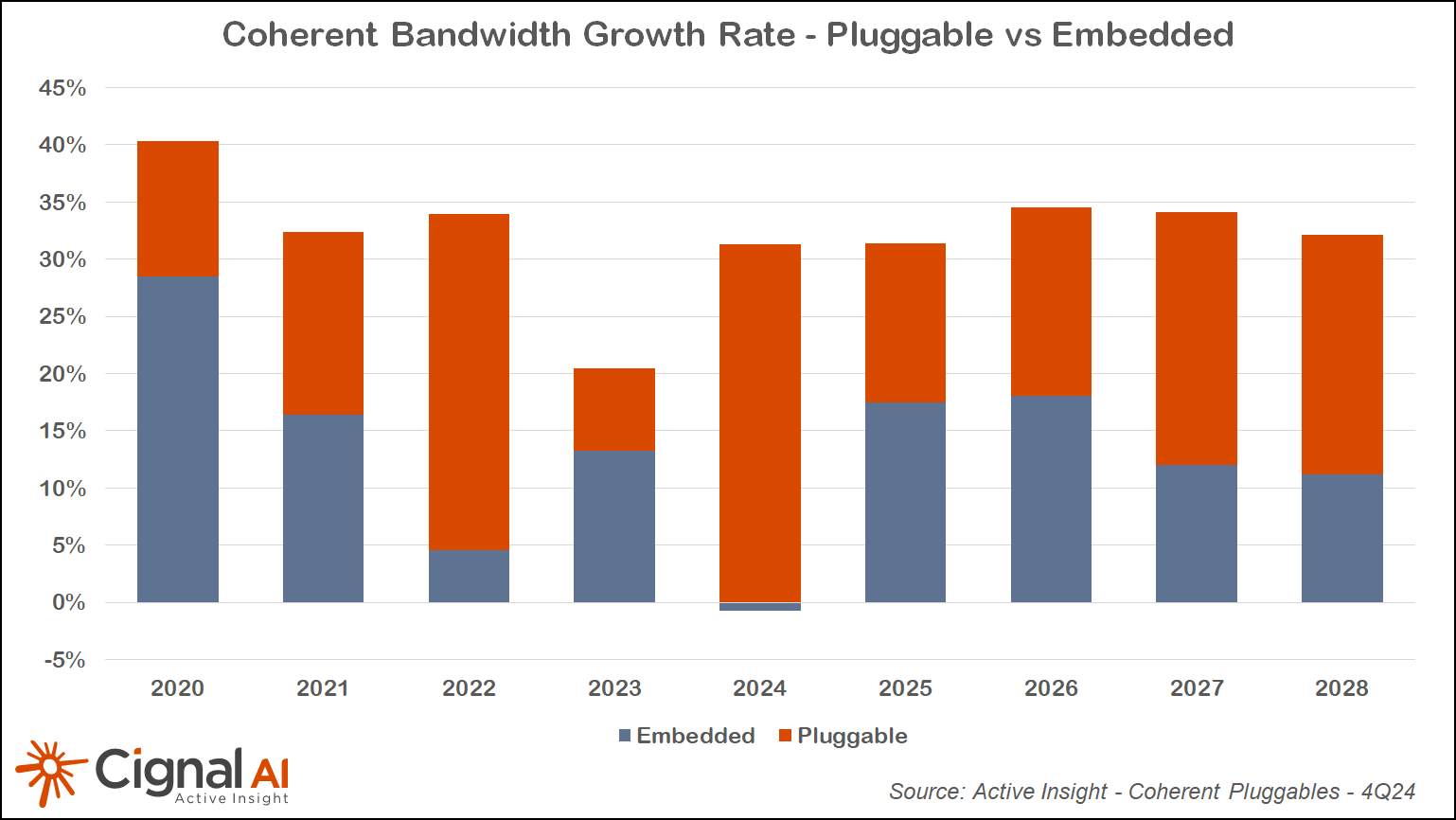

Coherent Optics: It’s a Pluggable World (1Q26)

In this update to our 1Q25 report, we cover the trends favoring pluggable optics as well as the companies positioned to benefit.

3Q25 Optical Component Report

Datacom revenue passed $5B with 800GbE module growth. Telecom revenue reached a 4-year peak with pluggable coherent modules and components.

ECOC 2025 Show Report

The Four Horseman of AI scaling: CPO, OCS, 1.6T, and 800ZR/Coherent Lite

2Q25 Optical Component Report

Datacom revenues and module shipments roared back from last quarter’s pause and Telecom revenue has recovered. 400ZRx pluggable shipments have slowed, but embedded high speed coherent made up the difference in deployed bandwidth.

AI Coherent Transport – Where are we Now?

Acacia examines the role of coherent pluggable optics in the roll out of AI training

1Q25 Optical Component Report

Datacom revenues and shipments slowed, 400ZRx shipments kept Telecom revenue growing for a fourth consecutive quarter.

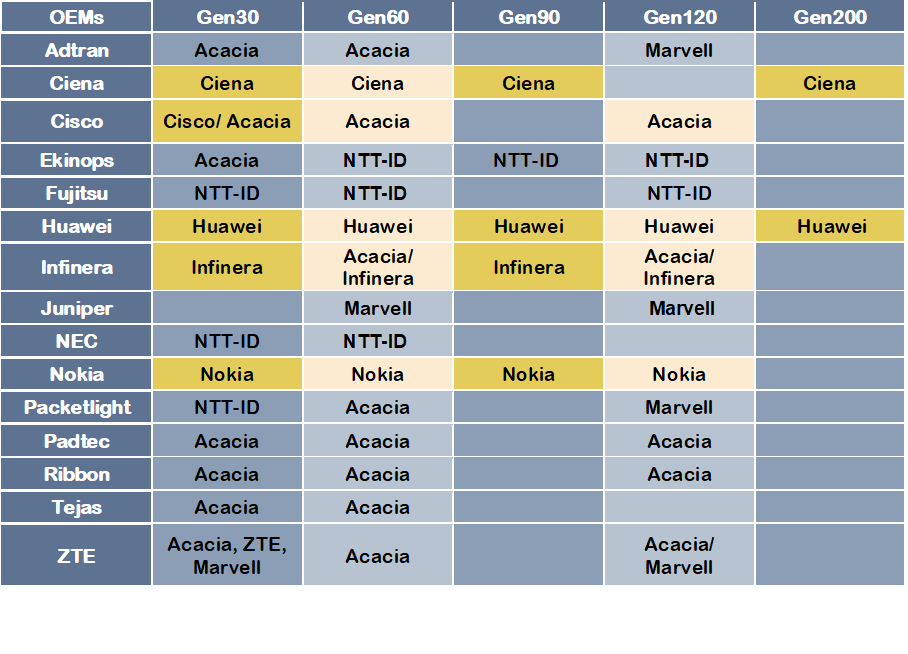

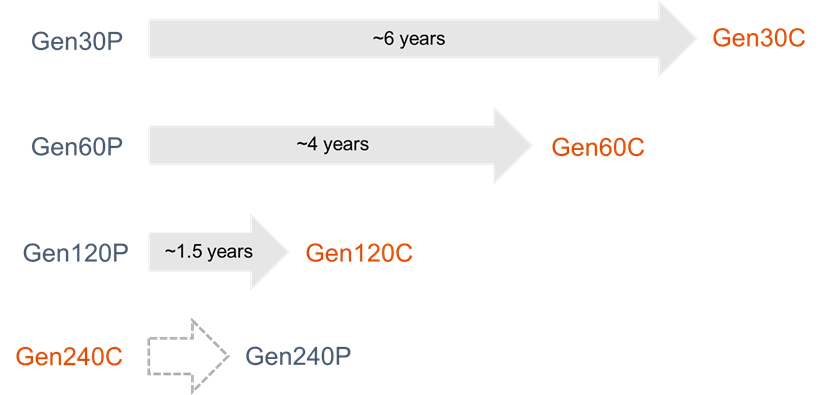

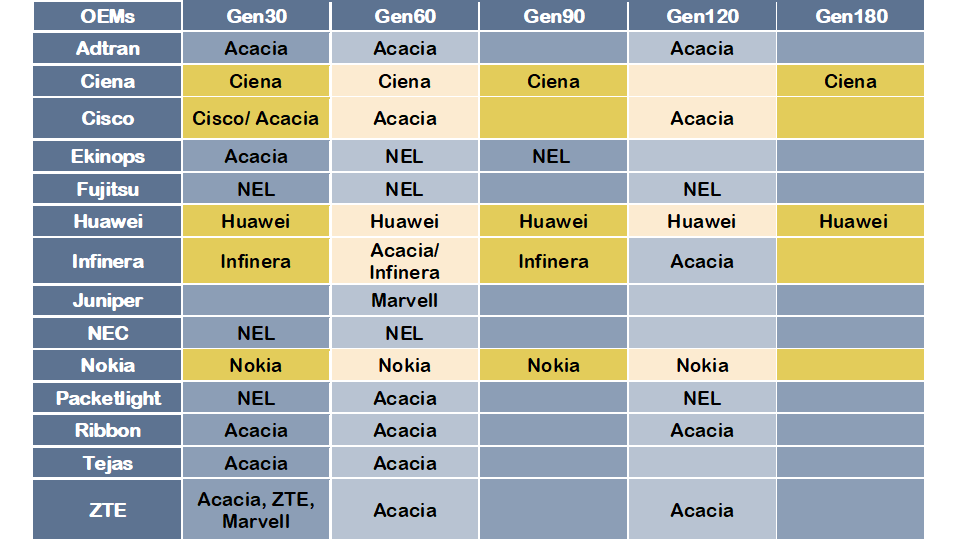

Tracking the Coherent DSP Supply Chain – 2025

Uncovering who uses which DSP, and which DSP vendors ship the most volume.

4Q24 Optical Component Report

Datacom revenue and port shipments stalled this quarter. Telecom revenue recovered from the doldrums based on 400G pluggables.

4Q24 Interim Optical Component Report

Final report will be issued once all Chinese companies complete 4Q24 reporting.

Coherent Optics: It’s a Pluggable World

Coherent pluggable optics were responsible for all the telecom bandwidth growth in 2024, and will account for most of the future growth.

3Q24 Optical Component Report

Datacom revenue more than doubled for the second quarter in a row as AI demand for 400GbE and 800GbE modules continued unabated. Telecom revenue has emerged from the depths of its recent decline.

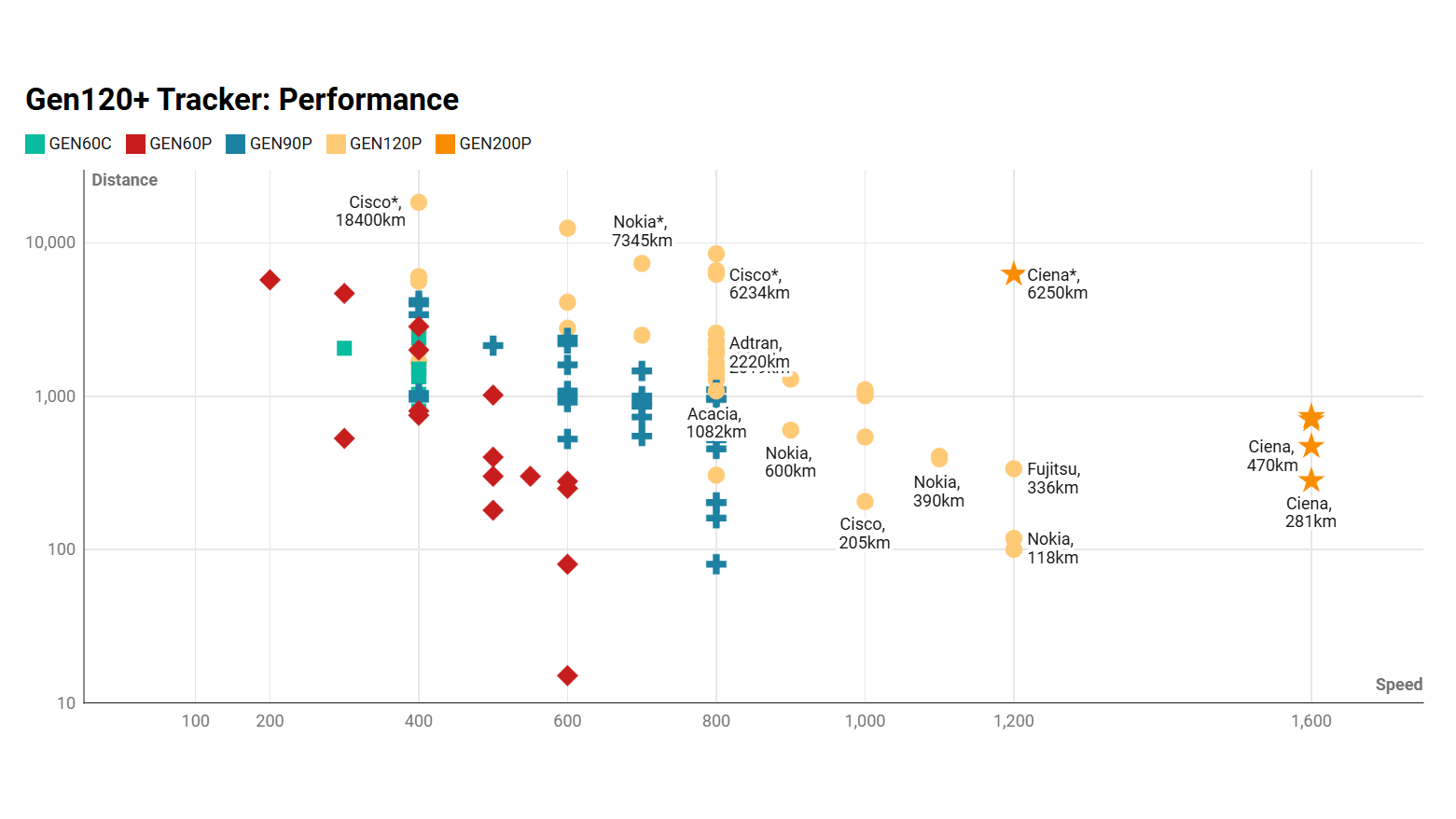

GEN120+ Coherent Trials and Deployments

Cignal AI is tracking announcements of Gen120 (120+ GBaud, 1+Tbps) optical trials and deployments.

ECOC 2024 Show Report

Nvidia PAM-4 DSP, Ciena 2x 800G-LR, LPO Lives, 1600ZR slipping, L-Band ramping.

Cisco Packet Optical Networking Conference 2024

Routed Optical Networking Goes Mainstream at Cisco’s PONC 2024. Our thoughts on the customer testimonials, product and technology updates, and live demonstrations.

CIOE24: Insights into China’s Market

Gathering the Chinese perspective on vendors and technologies.

2Q24 Optical Component Report

Datacom revenue hit new records with a surge in 400GbE shipments and continued growth in 800GbE. Telecom’s only growth area is 400G coherent pluggables.

IP-over-DWDM Pluggables Forecast

IP-over-DWDM deployments of 400/800/1600ZRx optics and adoption across market segments

Tracking the Coherent DSP Supply Chain

Uncovering who uses which DSP, and which DSP vendors ship the most volume.