4Q22 Weekly Earnings – META GOOG AMZN GLW JNPR MTSI

Cloud capex outlook for 2023 summarized

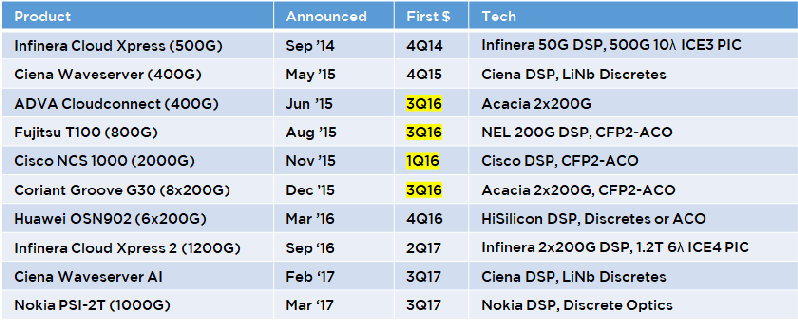

OFC21: 800G Coherent and Beyond

Several vendors are shipping 800Gbps capable coherent optical solutions, and now the industry must consider the next steps in development.

OFC2019 – Open and Disaggregated Networks

Open and disaggregated network equipment, software, and standards were a common theme on the floor and in presentations at OFC this year.

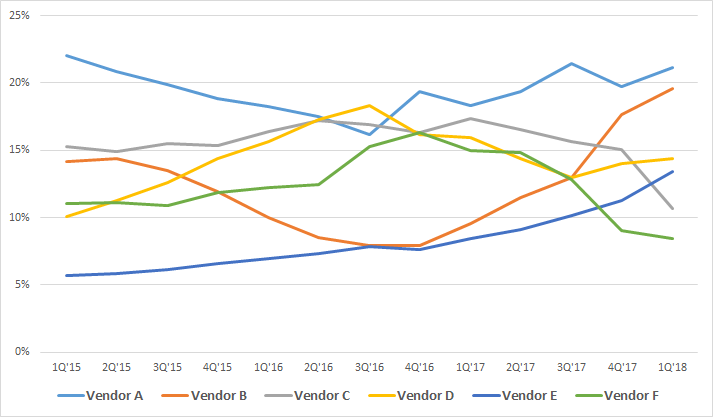

Cloud Spending on Optical Hardware – 1Q18 Update

In October 2017, Cignal AI analyzed the occurrence of a slowdown in spending by cloud & colo operators and quantified the magnitude of its impact (see Analysis: 1H17 Cloud and Colo Spending Slowdown).

Analysis: 1H17 Cloud and Colo Spending Slowdown

Cignal AI’s recent Optical Customer Markets Report discovered an unexpected weakness in 2017 optical transport equipment spending from cloud & colo operators (see Cignal AI Reports Unexpected Drop in Cloud and Colo Spending). This surprising trend was then further supported by public comments later made by Juniper and Applied Optoelectronics, prompting us to examine the situation in greater detail.

Nokia 2Q17

Nokia released its 2Q17 results on July 27th 2017. Cignal AI’s summary and analysis includes:

Overview of Quarterly Results

Cloud & Colo Business Update

OFC 2017 – Open vs. Closed Optical Networks

There was a new cult this year at OFC, the ‘Cult of Open.’ It formed from rising sentiment that the lack of interoperability of vendors in optical networks is a major…

OFC 2017 – Inside the Datacenter

100G and the Road to 400G

The transition to 100G network speeds inside the data center is underway at every major hyperscale operator simultaneously, creating major industry bottlenecks. Despite QSFP28…

Investor Call – OFC 2017 Takeaways

Andrew Schmitt provided key OFC 2017 takeaways during an investor call hosted by Troy Jensen of Piper Jaffray.