In the past, when coherent optics were reserved for long haul routes and high-capacity metros, the vertically integrated vendors who controlled their own DSPs (e.g., Ciena, Huawei, Infinera, Nokia) had the most success selling coherent optical ports. But as coherent optics have moved to pluggable formats and 400ZR-type modules have exploded in popularity for datacenter interconnect, that maxim no longer holds true. DSP development for high-performance optics supporting long-distance networks will remain within vertically integrated companies, but the market for the DSPs used in pluggables is expanding, with 800ZRx forecast to ship more than 200k ports in 2026 and 1600ZRx coming in 2027.

Growth in the coherent optical market has moved to pluggables, which now dominate the number of modules shipped. The cost of developing newer high speed performance modules is getting progressively higher, and the market is increasingly cannibalized by pluggables. As a result, more investment is going into higher performance pluggable DSPs, with 800ZR+ as the first coherent pluggable DSP designed specifically for long-haul and the upcoming (2027/8) 1600ZR+ DSP expected to handle all but the most demanding routes.

At 400G, two vendors (Acacia and Marvell) dominated the DSP market. The battle for 800G pluggable market share will be much more competitive, as OEM vendors like Ciena and Nokia are determined to take share at 800G. With Marvell’s first DSP not offering OpenROADM standard PCS, it will not be a part of the early volumes at Meta, which will be shared by Cisco, Ciena, and Nokia. It remains to be seen if Marvell’s respin – along with its large partnership base – will allow it to catch up in later years.

This report is an update to our annual report, last published in May 2025. It examines the market share for coherent DSPs. For information on the total volumes shipped of each coherent solution, a breakdown of module types, and forecasts for future growth, please refer to Cignal AI’s latest Optical Components Report.

Clients login to access

Purchase ReportBackground

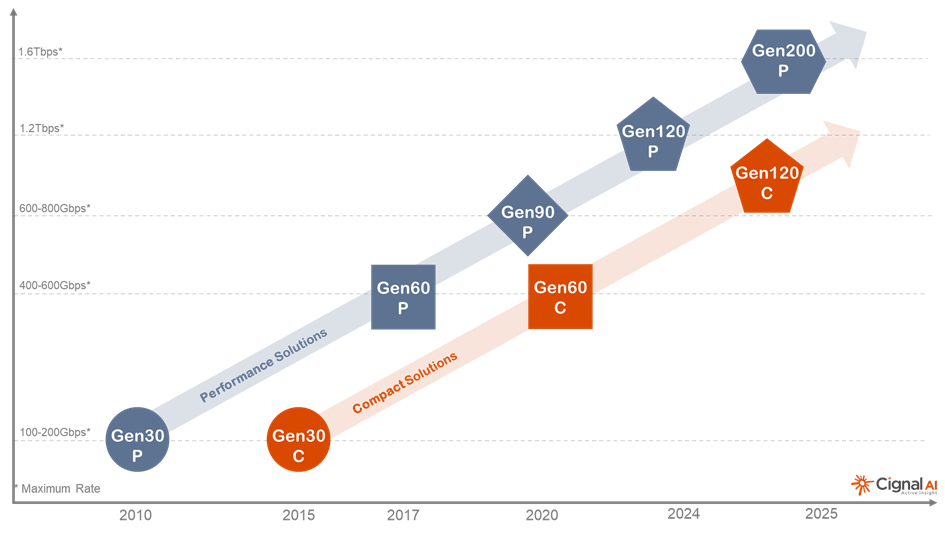

Cignal AI classifies coherent interfaces as a generation based on the baud rate (symbol transmission rate) of the technology. Within each generation, coherent technology is classified as Performance (P) or Compact (C). Performance optics are generally embedded solutions used for long-haul systems and compact solutions are lower-power and pluggable.

- Gen30 optics have a top speed of 100-200Gbps

- Gen60 optics have a top speed of 400Gbps (pluggable) and 400-600Gbp (embedded)

- Gen90 optics have a top speed of 800Gbps

- Gen120 optics have a top speed of 1.2Tbps (embedded) and 800G (pluggable)

- Gen200 optics have a top speed of 1.6Tbps

While higher speed (Gen240) optics have been announced, they have not yet been deployed and are not part of this report.

The DSP (Digital Signal Processor) is the brain behind coherent transmission; it decodes the complex signals that are sent over fiber and compensates for impairments like dispersion. As the baud rates rise, the DSP gate count and its feature complexity increase, which requires the latest generation process technologies.

Equipment OEMs

The table below lists OEM equipment vendors and the DSPs they use (or used to use in the case of Infinera). Highlights indicate a solution from a vertically integrated vendor that uses an internally developed DSP.

For many of the non-vertically integrated OEMs listed, the availability of standard, interoperable pluggable modules means that they are more flexible in the choice of DSPs. Vendors like PacketLight and SmartOptics may be using third-party pluggables based on Acacia today but will likely move to a multi-source supply chain as the pluggables become commonly available from multiple sources.

Clients log in to access full report