400 and 800GbE module shipments jump more than 25% QoQ

BOSTON (June 11, 2024) – Hyperscale network operator demand drove purchases of 400GbE and 800GbE datacom and 400ZR telecom optical modules to record levels, according to the 1Q24 Optical Components Report from research firm Cignal AI. Well over 3 million high-speed datacom modules were shipped this quarter in support of AI cluster interconnect and traditional computing applications.

“800GbE vendor shipments have yet to match demand, though nearly as many 800GbE modules shipped in 1Q24 as in all of 2023,” said Scott Wilkinson, Lead Analyst at Cignal AI. “While some vendors have reported that lead times are coming down, the demand for 400GbE and 800GbE modules remains exceptionally strong and we anticipate that datacom segment revenue will double in 2024.”

Additional 1Q24 Optical Component Report Findings:

- Spending on Datacom optical components was up more than 90% YoY as AI applications of 400GbE and 800GbE optical modules for AI applications drove demand to record levels.

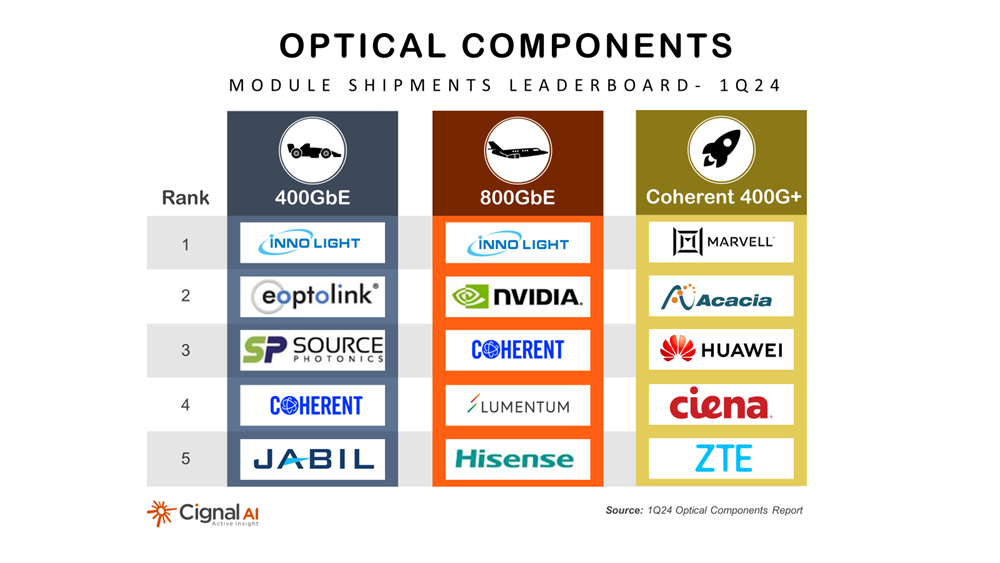

- Combined unit shipments of 400GbE and 800GbE Datacom modules across all SR/DR/FR/LR specifications jumped over 25% QoQ. Innolight led all vendors in shipments of Datacom modules.

- Telecom optical module shipment growth was concentrated in 400G coherent pluggables, which were up more than 35% YoY. Marvell and Acacia experienced strong shipment growth.

- Outside of pluggable coherent, shipments of Telecom components declined YoY, with segment revenue dropping -26% YoY.

- The coherent module market size declined to under $5 billion in 2023 but it will grow in 2024 and is expected to approach $10 billion in 2028.

Live Presentation Available

Results from Cignal AI’s Optical Components Report are presented live each quarter by Lead Analyst Scott Wilkinson. Clients are welcome to register for a presentation on June 18th at 11 AM ET.

About the Optical Component Report

Cignal AI’s Optical Components Report is published quarterly and provides revenue-based market share of company sales into four optical component markets – Datacom, Telecom, Industrial, and Consumer.

The report also tracks detailed unit shipments of Datacom and Telecom components, including 400GbE/800GbE/1.6TbE Datacom transceivers used for short-reach applications as well as pluggable and embedded coherent transceivers for Telecom applications. Five-year forecasts are also provided for all revenue segments as well as unit shipments.

Companies included in the report are Acacia, Accelink, Adtran, ADVA, Applied Optoelectronics, Broadex, Ciena, Cisco, Coherent, Emcore, Eoptolink, Fiberhome, Finisar, Fujitsu, Furukawa Electric, HG Genuine, Huawei, Hisense Broadband, Infinera, Innolight, Inphi, Intel, IPG Photonics, Jabil, Lumentum, Marvell, Mitsubishi, Molex, NEC, Neophotonics, Nokia, OE Solutions, PacketLight, SONT Technology, Source Photonics, Sumitomo, Sumitomo Osaka Cement, and ZTE.

A full description of the report methodology including an up-to-date listing of all product categories, as well as reports and presentations, are available on the report page.

About Cignal AI

Cignal AI provides active and insightful market research for the networking component and equipment market and the market’s end customers. Our work blends expertise from a variety of disciplines to create a uniquely informed perspective on the evolution of networking communications.

Contact Us/Purchase ReportSales: [email protected]

Web: Contact us